Financial Planning Fridays #18: The Yeild Curve

Today we wanted to talk with you about the yield curve and how it impacts where and how you should be allocating your money kept in cash and bonds.

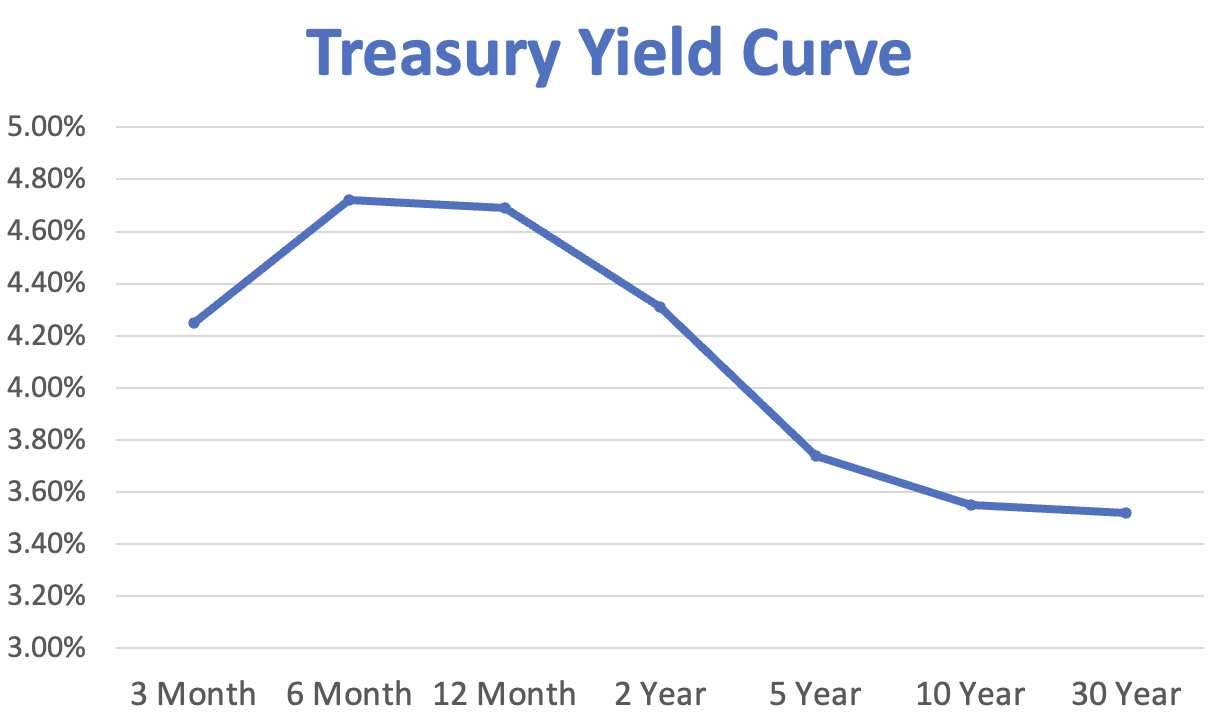

The yield curve is an illustration that shows the interest rates of bonds at different maturity dates. A maturity date is more simply known as the date on which you will receive your return of principal for any money you’ve invested in a bond.

Typically, in the yield curve we see most often, the further out the maturity date of the bonds, the more annual interest that bond pays the investor. This rewards you for taking on the risk of holding a bond until a date well into the future where the unknowns of interest rate movements come more into play.

However, as of December 8th, 2022, this is what the treasury yield curve looks like:

As you can see, this yield curve looks very different from the more common one.

It’s currently inverted, which means that investors are being paid more to hold their bonds for a shorter period of time than a longer one.

We see this type of curve most often when investors believe that rates may begin to fall in the future, and they are consequently comfortable locking in a lower rate for a longer maturity.

As demand for these long-term bonds go up, the price goes up accordingly. Because a bond’s yield is inversely correlated to its price, the yield curve inverts.

As you can see, a 1-year Treasury Bill is yielding about 4.7% while a 30-year Treasury Bond is only yielding about 3.5%.

Because of this, and wanting to maintain flexibility, we at Presilium are continuing to keep the bond portion of our client’s accounts in short-term, high quality bonds.

This is a situation that we will continue to monitor and evaluate for you as we look for an opportunity to increase the yield on your bond positions.

We also wanted to call attention to a recent article published in the Wall Street Journal: The $42 Billion Question: Why Aren’t Americans Ditching Big Banks?

Similar to our discussion in Financial Planning Fridays # 13, the article highlights how the American public is unfortunately earning much less interest on their savings than they probably should be. While the five largest banks in the US hold nearly 50% of all funds kept in banks, they were only paying an average of 0.40% on those deposits – a missed opportunity totalling nearly $42 billion in interest for those Americans!

Be on the lookout for our next Financial Planning Fridays episode. Subscribe to our Youtube Channel so you never miss an episode. Or contact us directly; schedule your 15-minute call with us today.